You might see a list of experienced bookkeepers or accounting organizations offering basic to premium bookkeeping services online and on-site as well. But are they offering what you actually need? Are you aware of the essential bookkeeping checklist that can streamline your organization?

To answer these questions, I have written a comprehensive guide personalized as per your business requirements. The Pro Accountants experts know that running a small business or a large enterprise requires strong grip on a lot of things, financials being the top.

We know that proper financial management is the backbone of any successful business but unfortunately, many business owners find themselves bogged down in the nitty-gritty details of their finances. They are so unsure of how to maintain accurate records, keep up with compliance, or streamline their processes that they end up taking poor decisions.

Being a decision maker, any confusion, the worry about errors, or the constant race against deadlines can lead you to mistakes that could cost your business time and money. To avoid this kind of scenario, you need to bring clarity to your processes like a structured, well-thought-out bookkeeping checklist that covers all essential tasks on a daily, weekly, monthly, and yearly basis.

Now let’s just discuss the common challenges and the ways to overcome those with proper knowledge or assistance from the experts.

The Struggle of Managing Your Business Finances

Imagine it’s the end of the month, and you’re sitting down to review your firm’s financial statements. You have a pile of receipts, invoices, and bank statements in front of you. Some transactions don’t match up. A payment was missed, and now there’s a late fee. On top of that, tax deadlines are around the corner, and you still haven’t reconciled your accounts. You start to feel the pressure of the task ahead.

This scenario is all too common for business owners and managers. Bookkeeping can quickly become overwhelming, especially without a structured system in place. The absence of a solid checklist to guide you through the process leads to errors, missed opportunities, and a lot of unnecessary stress. You may even find yourself questioning whether you’re on top of all the financial tasks required to keep your business running smoothly.

This is where an organized bookkeeping checklist or an expert advice can make all the difference.

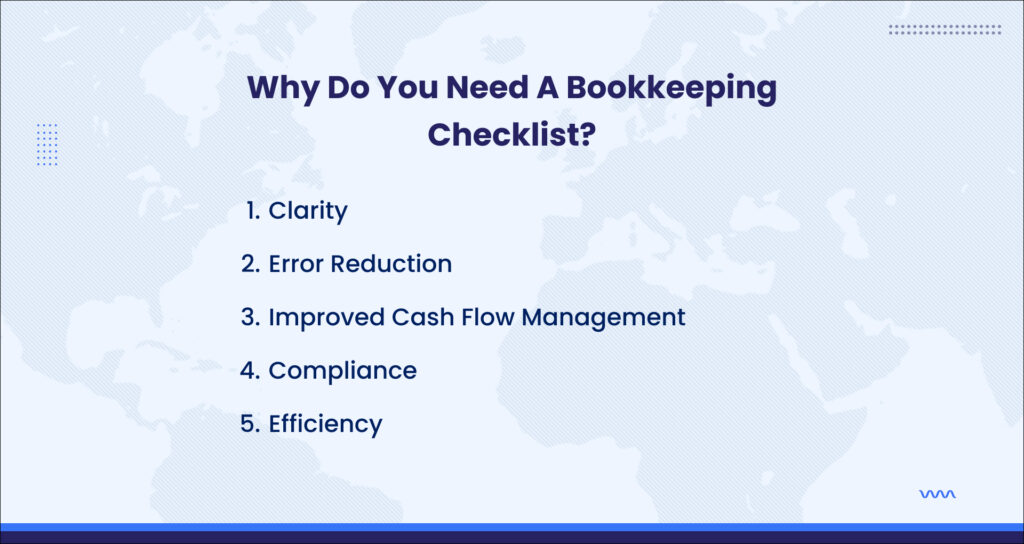

Why Do You Need a Bookkeeping Checklist?

At its core, a bookkeeping checklist is a structured way to ensure that every aspect of your firm’s finances is covered on a regular basis. Instead of playing catch-up or dealing with financial surprises, you can systematically address financial tasks and prevent issues before they arise. Other than that, you will get the following perks:

Clarity and Focus

A checklist breaks down complex financial tasks into smaller, manageable steps. This helps reduce overwhelm and allows you to focus on what needs to be done now versus what can wait.

Error Reduction

One of the biggest risks of unorganized bookkeeping is errors. A checklist ensures that every essential task is completed, reducing the chance of mistakes like miscalculations or missed payments.

Improved Cash Flow Management

Consistent financial tracking means you always have a clear understanding of your cash flow. You can plan better, make informed decisions, and avoid cash crunches.

Compliance and Timeliness

Staying compliant with tax laws and meeting deadlines becomes easier when you have a structured plan to follow. You won’t miss deadlines or incur penalties for late filings.

Efficiency

Having a checklist means less time is wasted on trying to figure out what needs to be done. You’ll know exactly what tasks to tackle and when, which boosts overall efficiency.

With the benefits clear, let’s move on to what tasks should be included in your daily, weekly, monthly, and yearly bookkeeping checklists.

Your Every Action Matters

Keeping up with daily financial tasks is essential to maintaining a healthy business. These are the routine jobs that ensure your firm’s financials remain up-to-date and accurate.

Small mistakes, like missing an expense or forgetting to invoice a client, can compound over time if not caught early. You should do the following practices:

Record Income and Expenses – Every day, make it a habit to record any new transactions, whether it’s income from clients or expenses like office supplies. This ensures that nothing slips through the cracks.

Track Payments and Receivables – Keep track of any payments that are due and ensure that your receivables are collected promptly. This helps maintain your cash flow.

Monitor Your Cash Flow – By staying aware of your cash flow daily, you can anticipate any shortages or surpluses and plan accordingly.

By completing these daily tasks, you’ll have a real-time view of your firm’s financial health, enabling better decision-making throughout the week.

Weekly Financial Management to Stay on Top of Recurring Tasks

Your weekly bookkeeping checklist should focus on reviewing your finances in greater depth and handling tasks that don’t need to be completed every day.

Weekly financial reviews help you identify patterns, correct small mistakes from your daily bookkeeping, and ensure that recurring obligations like payroll or vendor payments are handled on time.

Key Weekly Tasks Include:

- Make sure your bank account balances match your records. Reconciliation helps catch errors such as double payments or missed transactions early.

- Go through your vendor invoices and ensure payments are made on time. Late payments can affect your relationships with vendors and lead to late fees.

- If you run payroll on a weekly or bi-weekly basis, ensure that all timesheets are accurate and that employees are paid on time.

- Take time to review key reports, such as profit and loss statements or balance sheets. These reports give you a snapshot of your firm’s financial status.

By conducting these weekly checks, you can prevent financial surprises and keep your firm’s operations running smoothly.

Monthly Financial Tasks for a Broader Review

At the end of each month, it’s important to take a step back and review your firm’s financial performance on a larger scale. Monthly financial tasks give you an opportunity to correct any errors, adjust your financial strategy, and prepare for future growth.

Things that you need to focus on each month are to reconcile credit card statements same as you do for your bank accounts. Your credit card statements should be reconciled monthly as this ensures that all transactions are accounted for and helps catch any fraudulent charges.

Secondly, you need to review budget and your actual income as this allows you to adjust your financial plan if necessary and understand where your firm is overspending or underspending.

Thirdly, prepare financial statements at the end of each month. Generate financial statements such as income statements, balance sheets, and cash flow reports as these documents are critical for understanding the health of your firm and for reporting to stakeholders or lenders.

Finally, review your accounts receivable and payable to ensure that all outstanding invoices are collected and all due payments are made. This helps maintain a healthy cash flow and strengthens relationships with clients and vendors.

Completing these monthly tasks will give you a clear picture of your firm’s overall financial performance and ensure that you’re on track to meet your goals.

Annual Bookkeeping Tasks

As the year comes to a close, it’s time to review your firm’s finances on a yearly basis. Yearly bookkeeping tasks are larger, more strategic tasks that help you prepare for tax season and set the stage for the upcoming year.

The Role of Annual Bookkeeping

Your annual financial review gives you a comprehensive overview of your firm’s performance. It also allows you to plan for the future by setting new financial goals and preparing for tax filings.

Essential Year-End Tasks Include:

Prepare for Tax Filing

Review all your income, expenses, and deductions for the year to ensure that your tax filings are accurate. This is also a good time to meet with a tax professional to discuss any potential tax savings strategies.

Conduct a Full Financial Review

Review all of your financial statements from the past year to understand your firm’s overall performance. This will help you identify areas for improvement and set new financial goals for the upcoming year.

Adjust Budgets for the Next Year

Based on your financial performance, adjust your budget for the coming year. This ensures that your spending aligns with your firm’s financial goals.

Review and Update Insurance Policies

Review your firm’s insurance policies to ensure that you have adequate coverage for the coming year. This includes business liability, property, and health insurance for employees.

By completing these annual tasks, you’ll be prepared to enter the New Year with a clear financial strategy in place.

Overcoming Common Bookkeeping Challenges

Every firm, regardless of its size or industry, faces challenges when it comes to managing finances. While a structured bookkeeping checklist can help mitigate many of these issues, it’s important to recognize the specific challenges that firms often encounter.

The most common bookkeeping challenges that many businesses face include a variety of critical issues, each impacting the efficiency and accuracy of financial management.

One of the primary challenges is time management. Business owners often struggle to find sufficient time to keep up with daily or weekly bookkeeping tasks. This can result in financial records falling behind, leading to errors and missed deadlines that may complicate other aspects of the business. The second challenge is a lack of expertise. Not all firms have the in-house knowledge to manage their books accurately, and this gap can lead to mistakes, missed tax deductions, and even compliance issues that could be costly or disruptive.

Another major challenge is cash flow management. Poor cash flow oversight is one of the most significant financial hurdles businesses face. Without a clear understanding of cash flow, companies risk running into financial troubles, even if they are otherwise profitable. Additionally, compliance issues present a challenge, as tax laws and financial regulations are often complex and constantly evolving. Staying compliant requires an in-depth understanding of these rules, which many firms simply do not possess.

The key to overcoming these challenges lies in maintaining organization, establishing a structured bookkeeping process, and seeking professional assistance when necessary. For firms that struggle to keep up with their financial tasks, outsourcing to a professional service like The Pro Accountants can be transformative.

By outsourcing financial management, firms can ensure that all bookkeeping tasks are handled accurately and promptly. This approach allows business owners to focus on growth rather than worrying about financial record-keeping.

Wrapping Up

Staying on top of your firm’s finances doesn’t have to be stressful. By following a structured bookkeeping checklist, you can ensure that every aspect of your firm’s financial management is covered, from daily tasks to yearly reviews.

If you’re feeling overwhelmed or simply want to improve your firm’s financial processes, consider partnering with The Pro Accountants. Our team of financial experts can help you streamline your bookkeeping, improve cash flow management, and ensure compliance with all tax laws and regulations.

Ready to take control of your firm’s finances? Schedule a meeting with The Pro Accountants today, and let us show you how we can help you streamline your bookkeeping and set your firm up for long-term success.

Frequently Asked Questions

What is the benefit of having a daily bookkeeping checklist?

A daily bookkeeping checklist helps you maintain a close watch on your income, expenses, and other critical financial transactions in real-time. By updating your records every day, you can quickly catch and correct small errors before they escalate into bigger issues. Additionally, this routine allows you to track your cash flow daily, giving you insight into spending patterns and incoming revenue. A consistent daily approach also ensures that you are always audit-ready and can respond to unexpected expenses or opportunities with up-to-date financial data.

Why is reconciling bank accounts important?

Reconciling your bank accounts is crucial because it ensures your financial records align with your bank’s statements, catching any discrepancies, errors, or unauthorized charges. By reconciling frequently—ideally monthly—you have the opportunity to review all account activity, identify missing or duplicate entries, and correct mistakes early. Regular reconciliation also builds a strong foundation for accurate financial reporting, which is essential for audits, tax filings, and maintaining a clear picture of your business’s financial health.

How often should I review my financial statements?

Reviewing your financial statements at least once a month is essential to monitor your firm’s financial performance and track progress toward goals. Monthly reviews allow you to identify trends, such as consistent overspending in certain areas, early enough to take corrective action. Additionally, monthly checks ensure that you’re not faced with unexpected financial surprises at year-end. Yearly reviews, on the other hand, provide a comprehensive overview for tax preparation and strategic planning, giving you a high-level view to help guide long-term business decisions.

What is the purpose of a yearly bookkeeping review?

A yearly bookkeeping review gives you a full overview of your firm’s financial performance for the past year, which is invaluable for evaluating your business’s overall health. It prepares you for tax filings, as all transactions are reviewed, verified, and organized, which minimizes the risk of errors in your tax returns. A year-end review also lays the groundwork for next year’s budgeting and forecasting by highlighting areas where you exceeded or fell short of expectations, guiding more effective financial planning and goal-setting.

How can I improve my cash flow management?

Improving cash flow management involves closely monitoring your income and expenses, setting a structured review process, and frequently updating your accounts receivable and payable. Start by creating a forecast that projects your cash inflows and outflows, allowing you to anticipate periods when cash might be tight and plan accordingly. Automating invoicing and payment reminders can also speed up collections, reducing the amount of time cash is tied up in accounts receivable. Additionally, a well-organized bookkeeping system can help identify and reduce unnecessary expenses, further enhancing your cash flow stability.

What are the risks of falling behind on bookkeeping?

Falling behind on bookkeeping can lead to numerous issues, such as undetected errors, missed payments, and late tax filings, each of which can impact your business’s credibility and financial health. Without updated records, you lose visibility into your cash flow, making it harder to make informed decisions. This lack of oversight can result in missed tax deductions, penalties, and even compliance issues if regulatory deadlines are missed. In the long run, outdated bookkeeping can create chaotic financial records, which makes audits, tax preparations, and even day-to-day operations more challenging.

Can I outsource my firm’s bookkeeping tasks?

Yes, outsourcing bookkeeping is a practical solution that can save time, reduce errors, and allow you to focus more on core business activities. A professional bookkeeping service, like The Pro Accountants, offers the expertise to handle complex financial tasks, ensuring compliance, accuracy, and efficiency. Outsourcing can be especially beneficial if your firm lacks in-house financial expertise or if managing bookkeeping has become too time-consuming. By delegating these tasks, you gain access to specialized knowledge and tools, which can improve your financial management.

How do I know if my firm needs a professional bookkeeping service?

If bookkeeping is consuming more of your time than it should, or if you frequently find discrepancies in your financial records, it may be time to consider hiring a professional bookkeeping service. Common signs include falling behind on records, struggling with compliance, missing tax deductions, and experiencing difficulty managing cash flow. By working with professionals like The Pro Accountants, you can bring structure and accuracy to your financial management, allowing you to focus on growing your business rather than worrying about numbers.

What should I include in my monthly bookkeeping review?

Your monthly bookkeeping review should cover account reconciliation, financial statement analysis, budget comparisons, and updating invoices and payments. Start by reconciling bank and credit card statements to ensure all transactions are accurately recorded. Then, review key financial statements, such as income and expense reports, to assess performance and make adjustments if necessary. Check your budget against actual spending to track any variances. Finally, verify that all invoices are sent out and payments are collected, which helps maintain a healthy cash flow and prevents delays in receivables.

How do I get started with outsourcing my bookkeeping?

To start outsourcing your bookkeeping, the first step is to set up a consultation with a professional service like The Pro Accountants. During this meeting, your financial needs will be assessed, and a tailored plan will be developed to address your specific requirements. A reputable bookkeeping service will guide you through the transition process, including data transfer, system setup, and initial reconciliation. Once the system is in place, the service will manage your financial records, ensuring accuracy, compliance, and timely reporting while you focus on your core business activities.