With financial management playing a vital role in maintaining client trust and sustaining business growth, law firms must ensure their bookkeeping practices are accurate and transparent.

Unlike general businesses, law firms face unique financial challenges. From managing trust accounts to ensuring compliance with strict legal regulations, a minor oversight can lead to severe consequences, including financial penalties and reputational damage. Yet, bookkeeping often takes a backseat as firms prioritize client representation and case management.

In this blog, we’ll dive into the essentials of law firm bookkeeping, unravel the challenges unique to the legal sector, and provide actionable tips to set your firm up for success. Whether you’re managing a small practice or overseeing the financials of a large firm, these insights will help you streamline your processes, maintain compliance, and focus on what you do best—serving your clients.

Understanding Law Firm Bookkeeping Basics

Bookkeeping for law firms involves more than just tracking income and expenses—it’s about maintaining compliance with legal industry regulations while ensuring the financial health of the firm. To avoid legal penalties and reputational harm, law firms must adhere to strict standards, particularly when managing trust accounts and handling client funds.

What is Law Firm Bookkeeping?

At its core, law firm bookkeeping is the process of systematically recording, organizing, and managing the financial transactions of a legal practice. However, what sets it apart is the need to align these practices with stringent legal and ethical standards. These standards govern how client funds are handled, how financial records are maintained, and how compliance is demonstrated to regulators.

For instance, lawyers often deal with client retainers deposited into trust accounts, which must be managed separately from the firm’s operational funds. This separation is vital to prevent misuse or commingling of funds—a violation that could result in penalties, suspension, or even disbarment.

In addition, law firms must track revenue differently than standard businesses. Revenue often depends on case outcomes, which means income cannot always be recognized immediately. A robust bookkeeping system ensures that firms adhere to accounting principles while meeting regulatory requirements.

- Trust accounts, often referred to as Interest on Lawyer Trust Accounts (IOLTA), are a hallmark of legal bookkeeping. These accounts are used to manage client funds for expenses like court fees, settlements, or retainers. Mishandling trust accounts—even inadvertently—can lead to severe legal repercussions.

For example, if a firm accidentally uses funds from a trust account to cover operational expenses, this would be considered a breach of trust account regulations. Proper bookkeeping ensures that every transaction is accurately recorded and reconciled.

- Unlike many businesses that recognize revenue upon providing a service or delivering a product, law firms often work on cases where revenue is contingent upon milestones or final outcomes. For instance, contingency cases don’t generate revenue until a settlement or judgment is reached. Accurate bookkeeping helps firms track these nuances and avoid premature income reporting.

- Legal firms incur specific types of expenses such as filing fees, deposition costs, and legal research tools (e.g., LexisNexis or Westlaw). Categorizing these expenses properly is crucial for tax reporting and financial analysis. Misclassification can lead to overpayment of taxes or reduced profitability.

Legal billing relies heavily on tracking time. Distinguishing between billable hours (direct client work) and non-billable hours (administrative tasks, training) is essential for evaluating productivity and profitability.

The Importance of Compliance

One of the most critical aspects of law firm bookkeeping is compliance. Failing to comply with legal and financial regulations can lead to dire consequences. For example:

- Mismanagement of client trust accounts can result in fines, suspensions, or disbarment.

- Inaccurate financial reporting can trigger audits or investigations, damaging the firm’s reputation.

By keeping detailed and accurate records, law firms demonstrate their commitment to ethical practices. Moreover, well-maintained financial records protect against disputes with clients, regulators, or employees.

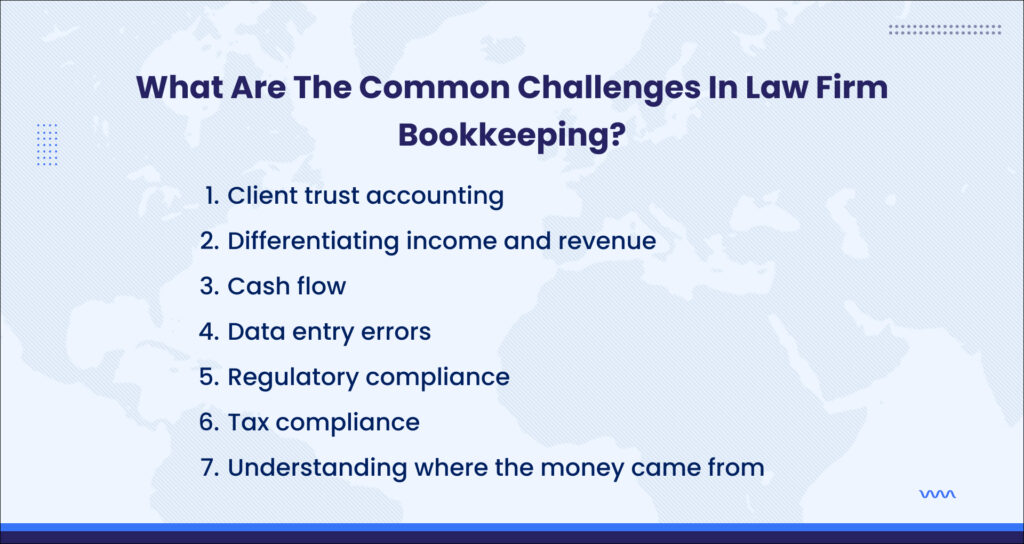

Common Challenges in Law Firm Bookkeeping

Bookkeeping for law firms comes with unique hurdles that can create significant operational and compliance risks if not managed correctly. These challenges often stem from the industry’s specialized requirements, such as:

- Trust accounting

- Billable hours tracking

- Compliance with regulatory frameworks.

Differentiating Between Operating and Trust Funds

While trust accounts manage client-specific funds, operating accounts handle the firm’s day-to-day expenses, such as salaries, utilities, and marketing. Keeping these funds distinct is not just a best practice but a legal requirement.

Challenges:

• Complex Transactions:

Lawyers often withdraw earned fees from trust accounts, requiring clear documentation to prevent errors.

• Regulatory Scrutiny:

Operating and trust funds are closely monitored by regulators. Mismanagement, even unintentionally, can trigger audits and fines.

Tracking Billable vs. Non-Billable Hours

Billable hours are the backbone of a law firm’s revenue, while non-billable hours reflect internal tasks such as administrative work or training. Differentiating and documenting these hours is essential for accurate client billing and productivity analysis.

Challenges:

• Time Leakage:

Without robust time-tracking systems, firms may underreport billable hours, leading to revenue loss.

• Disorganized Records:

A lack of clarity in timekeeping can result in client disputes or delayed payments.

Expense Categorization and Allocation

Legal firms deal with various expenses, including court fees, expert witness fees, and research subscriptions. Properly categorizing and allocating these expenses is crucial for tax purposes and financial analysis.

Challenges:

• Complex Expense Structures:

Some expenses, such as shared case costs, need to be divided among multiple clients or cases.

• Tax Implications:

Misclassified expenses can lead to inaccurate tax filings, overpayments, or missed deductions.

Staying Audit-Ready

Law firms are often subject to audits from bar associations or tax authorities. Inconsistent or incomplete records can make the audit process stressful and increase the risk of penalties.

Challenges:

• Inconsistent Record-Keeping:

Many firms lack a standardized process for recording transactions, leading to gaps or inaccuracies.

• Stressful Audit Preparation:

Preparing for an audit without comprehensive financial records can divert resources away from client work.

Actionable Strategies for Effective Bookkeeping in Law Firms

Addressing the unique challenges of law firm bookkeeping requires a strategic and tailored approach. By implementing modern tools, adopting best practices, and ensuring compliance with legal regulations, law firms can streamline their financial processes and focus on delivering value to their clients. Below are actionable strategies to optimize your law firm’s bookkeeping.

1. Leverage Legal-Specific Bookkeeping Software

Investing in software designed for law firms simplifies bookkeeping by automating tasks, ensuring compliance, and providing detailed financial insights.

Benefits:

- Trust Accounting Management: Tools like Clio Manage and QuickBooks for Lawyers offer features specifically for tracking client funds in trust accounts.

- Time Tracking Integration: Many software solutions integrate with time-tracking tools, ensuring accurate billing for all hours worked.

- Customizable Reporting: Generate financial reports tailored to your firm’s needs, aiding in decision-making.

Pro Tip: When choosing software, prioritize scalability to ensure it grows with your firm.

2. Implement Robust Time-Tracking Systems

Accurate time tracking is essential for maximizing billable hours and ensuring transparency in client billing.

Action Steps:

- Use cloud-based tools like Toggl or TimeSolv to track time spent on cases in real time.

- Train staff to log time daily, minimizing errors and forgotten entries.

- Regularly review time logs to identify patterns and improve efficiency.

Impact: Firms that implement automated time tracking report up to 10% increased revenue due to accurate billing.

3. Regularly Reconcile Accounts

Reconciling trust and operating accounts monthly (or more frequently) ensures that all transactions are accounted for and discrepancies are addressed promptly.

Best Practices:

- Cross-check bank statements against your bookkeeping records to identify errors or unauthorized transactions.

- Use reconciliation tools provided by your accounting software to streamline the process.

- Document reconciliation efforts to maintain an audit trail.

Result: Consistent reconciliation reduces the risk of overdrafts and compliance violations.

4. Outsource to Legal Bookkeeping Professionals

Hiring professionals who specialize in law firm bookkeeping can save time and reduce errors.

Advantages:

- Expertise in Regulations: Legal bookkeepers understand bar association rules and trust accounting requirements.

- Focus on Core Activities: Outsourcing frees up attorneys to focus on legal work rather than administrative tasks.

- Scalability: External services can handle increased bookkeeping demands as your firm grows.

Did You Know? According to a survey, outsourcing bookkeeping reduces operational costs by an average of 40%.

5. Create a Chart of Accounts for Legal-Specific Expenses

A detailed chart of accounts tailored to law firms helps categorize expenses accurately and simplifies tax filing.

Categories to Include:

- Client Costs: Filing fees, expert witness payments, etc.

- Office Expenses: Rent, utilities, and office supplies.

- Professional Services: Marketing, consulting, and legal research subscriptions.

- Payroll: Salaries and benefits for attorneys and staff.

Action Step: Review and update your chart of accounts annually to reflect changes in your firm’s operations.

6. Schedule Regular Compliance Audits

Proactively auditing your financial processes ensures adherence to regulations and identifies areas for improvement.

Steps for Effective Audits:

- Perform an internal audit quarterly to review trust account management and expense categorization.

- Engage external auditors annually for an unbiased assessment.

- Address audit findings immediately to prevent recurring issues.

Outcome: Regular audits reduce the likelihood of penalties and improve financial accuracy.

7. Set Clear Billing Policies

Transparent billing practices enhance client trust and minimize disputes.

Strategies:

- Use itemized invoices to show a breakdown of services and costs.

- Establish payment terms upfront, including retainer agreements and due dates.

- Offer multiple payment options, such as credit card payments or online portals.

Example: A law firm that adopted clear billing policies reported a 20% decrease in late payments within six months.

8. Train Staff on Bookkeeping Basics

Empowering your team with bookkeeping knowledge reduces the risk of errors and enhances collaboration.

Training Focus Areas:

- Trust account regulations and compliance.

- Proper documentation of transactions and expenses.

- Efficient use of bookkeeping software.

Bonus Tip: Provide ongoing training to keep your team updated on new tools and regulations.

9. Monitor Cash Flow Proactively

Cash flow management is vital for maintaining financial stability, especially for firms operating on contingency fees.

Steps to Take:

- Use cash flow forecasting tools to anticipate periods of low revenue.

- Establish a cash reserve to cover fixed expenses during slow months.

- Follow up promptly with clients on overdue invoices.

Result: Proactive cash flow management reduces financial stress and ensures operational continuity.

10. Stay Updated on Regulatory Changes

Legal accounting rules and tax laws evolve regularly. Staying informed prevents non-compliance and potential fines.

How to Stay Updated:

- Subscribe to newsletters from your state bar association or legal accounting bodies.

- Attend workshops or webinars focused on legal bookkeeping.

- Partner with a professional service like The Pro Accountants, which monitors regulatory updates on your behalf.

Impact: Firms that prioritize compliance updates report fewer instances of penalties or client disputes.

Real-World Statistics:

- Trust Accounting Violations: A 2023 survey by American Bar Association revealed that 45% of disciplinary actions against lawyers stemmed from trust accounting mismanagement.

- Technology Adoption: As per LegalTech Insights, law firms using legal-specific software reported a 25% increase in operational efficiency compared to firms relying on manual processes.

Enhancing Profitability and Efficiency Through Strategic Bookkeeping

Effective bookkeeping is not merely a back-office function; it serves as the backbone of a profitable and sustainable law firm. By leveraging the strategies mentioned earlier, law firms can achieve financial clarity, boost operational efficiency, and ultimately enhance profitability. Below, we explore the measurable benefits of strategic bookkeeping practices.

1. Improved Financial Visibility

Accurate and timely bookkeeping provides a clear snapshot of your firm’s financial health.

How It Helps:

- Identify trends in revenue and expenses, enabling better financial planning.

- Monitor the profitability of individual cases by analyzing associated costs and billable hours.

- Ensure sufficient funds are available for upcoming expenses, such as payroll and office overheads.

Outcome: Better financial visibility empowers decision-makers to allocate resources effectively and invest confidently in growth opportunities.

2. Enhanced Client Trust Through Compliance

Adherence to legal and financial regulations builds trust with clients and stakeholders.

How It Helps:

- Transparent trust account management reassures clients that their funds are handled ethically and responsibly.

- Accurate and detailed invoices minimize billing disputes, fostering positive client relationships.

- Regular compliance audits reduce the risk of reputational damage from legal penalties.

Impact: Firms that prioritize compliance often report higher client retention rates and stronger referrals.

3. Streamlined Operations

Efficient bookkeeping reduces administrative burdens, allowing attorneys to focus on their core responsibilities.

How It Helps:

- Automated time-tracking and billing systems save hours of manual work each week.

- Outsourcing complex bookkeeping tasks frees up internal resources for strategic initiatives.

- Proactive cash flow management eliminates the stress of scrambling for funds during lean periods.

Result: Streamlined operations lead to a more productive and satisfied team, directly impacting client service quality.

4. Better Financial Decision-Making

Data-driven decisions are crucial for long-term success, and well-maintained financial records provide the foundation for such decisions.

How It Helps:

- Analyze profit margins by case type or practice area to focus on high-yield services.

- Set realistic revenue targets based on historical performance and industry benchmarks.

- Evaluate the financial impact of hiring additional staff or expanding into new markets.

Example: A mid-sized law firm used detailed financial reports to identify underperforming practice areas, reallocate resources, and increase overall profitability by 15% within a year.

5. Reduced Costs Through Preventive Measures

Proactive bookkeeping can help law firms save money by avoiding penalties, interest, and inefficiencies.

How It Helps:

- Early identification of billing errors reduces revenue leakage.

- Accurate categorization of expenses maximizes tax deductions and minimizes audit risks.

- Eliminating manual processes reduces overhead costs associated with labor-intensive tasks.

Result: Cost savings are reinvested into growth areas like marketing, technology, or staff development.

6. Increased Scalability

As your law firm grows, having robust bookkeeping systems in place ensures seamless scalability.

How It Helps:

- Advanced software and professional services can handle higher transaction volumes without compromising accuracy.

- Scalable processes support the addition of new practice areas, attorneys, or office locations.

- Financial insights from well-maintained records guide expansion decisions, reducing risk.

Outcome: Firms equipped with scalable bookkeeping practices grow more efficiently and maintain profitability during expansion.

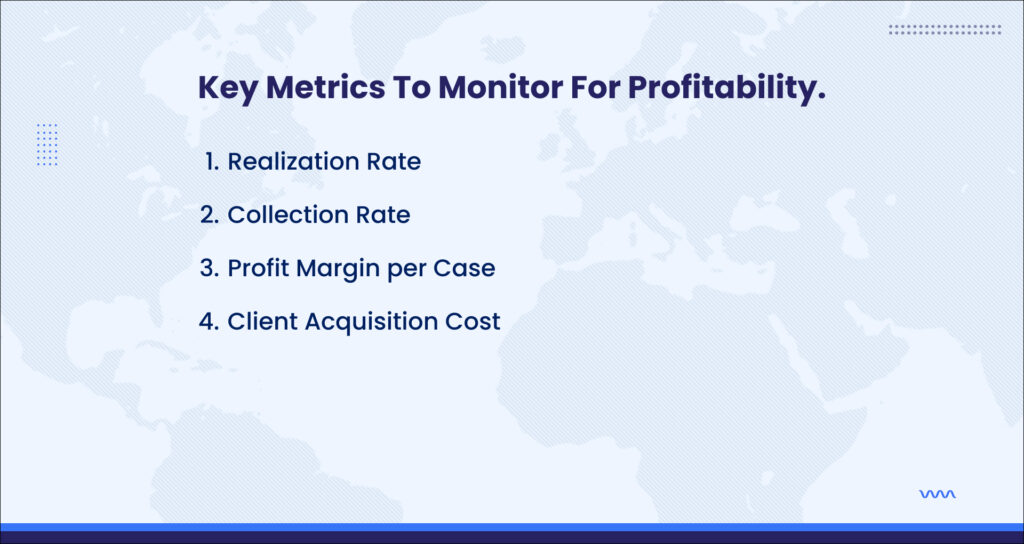

Key Metrics to Monitor for Profitability

To evaluate the effectiveness of your bookkeeping strategies, regularly track these metrics:

- Realization Rate: Percentage of billable hours collected as revenue.

- Collection Rate: Proportion of invoices paid by clients on time.

- Profit Margin Per Case: Net profit earned from each legal matter.

Client Acquisition Cost: Expenses related to acquiring a new client versus the revenue they generate.

Agitating the Pain Points

Without strategic bookkeeping practices, law firms risk:

- Missed Growth Opportunities: Lack of financial data can hinder expansion or investment decisions.

- Revenue Leakage: Poor billing practices can result in undercharging or unpaid invoices.

- Reputation Damage: Compliance violations or client disputes can erode trust and lead to client loss.

Success Story

A small law firm struggling with inconsistent cash flow and trust account mismanagement sought professional bookkeeping services. Within six months, they:

- Improved cash flow by 30% through proactive billing and collections.

- Passed a state bar audit with no compliance issues.

- Expanded their practice areas, thanks to actionable financial insights.

This transformation highlights the direct correlation between effective bookkeeping and a firm’s success.

Why Law Firms Need Professional Bookkeeping Services

As we’ve explored throughout this blog, effective bookkeeping is not just about maintaining accurate financial records; it’s about establishing a strong foundation for growth, compliance, and profitability. Law firm bookkeeping, in particular, requires attention to detail, specialized knowledge, and a commitment to accuracy, as mistakes or oversight can have serious consequences. The challenges are unique, but the solutions are clear—and investing in robust bookkeeping practices is a step every law firm should take to ensure long-term success.

By implementing the actionable strategies outlined, law firms can:

- Enhance Profitability: Streamlined financial operations and improved cash flow management lead to better financial outcomes.

- Build Client Trust: Transparent, compliant bookkeeping ensures clients feel secure in your firm’s handling of their funds.

- Achieve Scalability: Efficient bookkeeping systems support the growth and expansion of your firm without compromising financial integrity.

However, as we’ve seen, maintaining accurate and compliant books can be complex, especially for firms managing large volumes of transactions and trust accounts. This is where The Pro Accountants can make a significant difference.

At The Pro Accountants, we specialize in providing bookkeeping services tailored to law firms. Our team understands the specific requirements of legal accounting, from trust account management to accurate billing practices, and we are committed to ensuring that your firm remains compliant and financially sound.

Our Key Offerings Include:

- Comprehensive Bookkeeping: We manage your day-to-day accounting, including expense tracking, revenue generation, and trust account reconciliation, ensuring everything is in order for both financial management and audits.

- Financial Reporting: Detailed, easy-to-understand financial reports help you monitor profitability, optimize your billing process, and make data-driven decisions.

- Tax Compliance: Our experts ensure you remain compliant with tax laws, optimizing deductions and avoiding penalties.

- Customized Solutions: We work closely with you to design a bookkeeping system that meets your firm’s unique needs and scales as your practice grows.

The Pro Accountants Advantage:

- Industry Expertise: We have years of experience working with law firms and are well-versed in the regulations that govern legal accounting.

- Personalized Service: We take the time to understand your firm’s specific financial situation and tailor our services to meet your needs.

- Peace of Mind: With our team on your side, you can focus on what you do best—practicing law—while we handle the complexities of bookkeeping.

We offer a free consultation to assess your firm’s needs and provide customized solutions that will simplify your finances, improve your cash flow, and ensure compliance with legal accounting standards.

Schedule a Meeting with Us Today to discuss how we can help you transform your firm’s financial management and achieve your long-term business goals.

Frequently Asked Questions

What is law firm bookkeeping?

Law firm bookkeeping involves managing and recording a law firm’s financial transactions, including revenue from billable hours, client payments, and expenses. It also includes tracking trust accounts and ensuring compliance with legal and ethical standards.

2. Why is bookkeeping important for law firms?

Bookkeeping is crucial for law firms because it helps track income, manage expenses, ensure compliance with regulations, and provide financial insights for better decision-making. Proper bookkeeping ensures smooth operations and protects the firm from legal or financial risks.

3. What are trust accounts, and why are they important?

A trust account is a separate account where law firms hold client funds for specific purposes, such as settlements or retainer fees. Proper management of these accounts is essential to avoid violations of ethical and legal standards, ensuring transparency and client trust.

4. Can I manage my law firm’s bookkeeping on my own?

While it’s possible for a law firm owner to manage bookkeeping themselves, it can be time-consuming and complex. Given the unique requirements of law firm accounting (e.g., trust account management, compliance), many firms choose to hire professional bookkeepers or accountants with specialized expertise.

5. What are the most common bookkeeping challenges for law firms?

Common challenges include managing trust accounts accurately, ensuring timely billing and collections, staying compliant with legal regulations, handling complex revenue streams (e.g., hourly billing, contingency fees), and preventing financial errors or fraud.

6. How do I choose the right bookkeeping software for my law firm?

When choosing bookkeeping software, look for features tailored to law firms, such as trust account management, billing and invoicing capabilities, client payment tracking, and compliance with legal regulations. Popular software options for law firms include QuickBooks, Clio, and Timeslips.

7. How often should I reconcile my law firm’s trust accounts?

Trust accounts should be reconciled monthly to ensure that funds are handled correctly and that there are no discrepancies between the client’s records and your firm’s records. Frequent reconciliation helps maintain compliance and avoid issues during audits.

8. What are some signs that my law firm needs professional bookkeeping help?

Signs include inconsistent cash flow, difficulty tracking client payments or trust accounts, an increase in billing errors, or challenges staying compliant with tax regulations. Professional bookkeeping services can provide clarity and ensure your firm’s financial health.

9. How can accurate bookkeeping help with my law firm’s profitability?

Accurate bookkeeping helps identify profitable practice areas, monitor cash flow, reduce unnecessary expenses, and ensure that billing is correct. By analyzing financial data, law firms can make more informed decisions that improve profitability and sustainability.

10. How do I ensure my law firm is compliant with financial regulations?

Compliance requires maintaining accurate financial records, properly managing trust accounts, following industry-specific regulations, and filing taxes on time. Working with a professional accountant who understands the legal industry can help ensure your firm remains compliant.