What is Catch-Up Bookkeeping? A Guide to Its Function and Examples

You’re sitting at your desk, sipping your coffee, and the thought strikes you—you haven’t updated your financial records in months. Maybe you were too busy running your business or handling personal matters, and now, it feels like you’re drowning in a sea of transactions, invoices, and receipts. It’s overwhelming. You know you need to get things in order, but the idea of combing through months, or even years, of financial data feels like a mountain too high to climb.

You’re not alone. Many business owners and individuals find themselves in this exact situation, where staying on top of financial records simply slips through the cracks. Whether it’s because of a lack of time, knowledge, or simply procrastination, financial tracking often falls by the wayside. But now, it’s crunch time—tax season is looming, financial decisions need to be made, or perhaps a lender is asking for updated financial records.

This is where catch-up bookkeeping comes to the rescue. It’s designed for people like you, who may have fallen behind but want to get back on track. In this guide, we’ll dive into everything you need to know about this important process, from its function and benefits to real-world examples and practical advice on how to get started.

By the end of this journey, you’ll not only understand how catch-up bookkeeping works, but you’ll also see how it can ease the financial burden and give you peace of mind.

What Is Catch-Up Bookkeeping?

At its core, catch-up bookkeeping is the process of bringing your financial records up to date when you’ve fallen behind on regular tracking. It’s like hitting the reset button on your finances, allowing you to reconcile months (or years) of untracked transactions and reestablish clarity in your financial picture.

Think of your financial records as the foundation of your business or personal finances. When this foundation becomes shaky due to a backlog of unrecorded transactions, you’re left in the dark about your financial health. This is more than just a nuisance—without up-to-date financial records, you may be missing out on crucial information needed to make informed decisions.

Catch-up bookkeeping gives you the opportunity to rebuild that foundation, ensuring that every income, expense, and transaction is properly documented and reconciled. Whether you’re a small business owner needing to file taxes or an individual managing personal finances, this process provides a clear view of where you stand financially.

But let’s take it one step further—catch-up bookkeeping isn’t just about correcting past mistakes; it’s about preparing you for future success. Once you’ve caught up, you’re in a much better position to maintain ongoing financial health.

Why Do People Fall Behind on Bookkeeping?

The truth is, it happens to the best of us. Life gets busy. Running a business means juggling dozens of responsibilities, from managing employees to dealing with customers and suppliers. Amid all of this, keeping track of financial data can easily get pushed down the priority list.

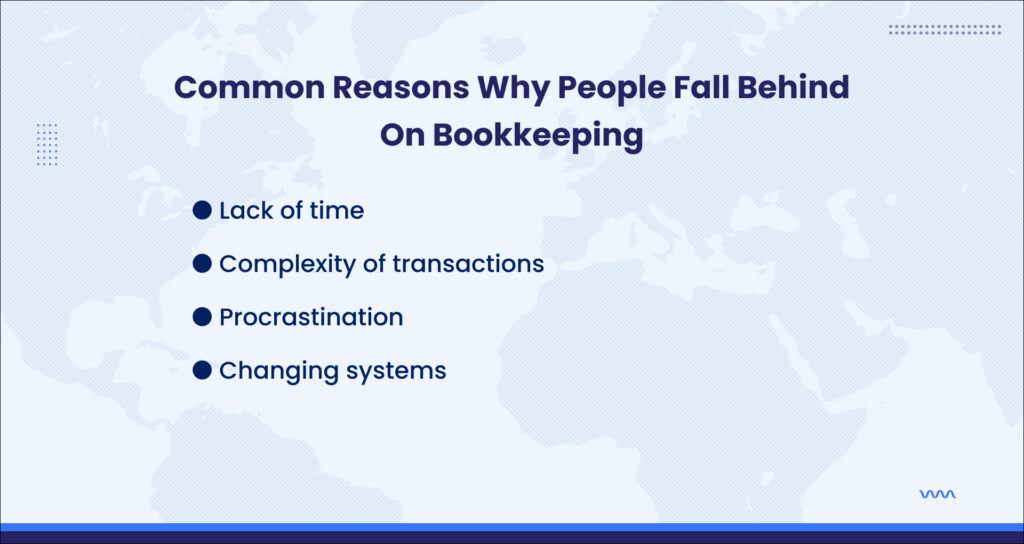

Here are a few common reasons why people fall behind:

- Lack of time: Entrepreneurs are often wearing multiple hats, and staying on top of financial records requires time and attention that they simply don’t have.

- Complexity of transactions: As businesses grow, so does the complexity of financial transactions. This can make it difficult to manage financial records without professional assistance.

- Procrastination: Some people delay financial tracking because they find it tedious, or they might feel intimidated by the numbers.

- Changing systems: Switching accounting systems or processes can lead to confusion and gaps in record-keeping.

How Does It Differ from Regular Bookkeeping?

Catch-up bookkeeping differs from regular financial management in that it focuses specifically on addressing past gaps in your financial records. While regular financial tracking is proactive and ongoing, catch-up work is retroactive. You’re looking back to reconcile what has already happened rather than focusing on current transactions.

When you’re keeping up with financial records regularly, it’s relatively easy to stay organized and maintain accuracy. But when you fall behind, catching up requires more time, effort, and attention to detail. You’ll need to dig through old receipts, bank statements, and invoices to ensure that nothing is missed. Depending on how far behind you are, this process can be quite labor-intensive.

But the goal remains the same: To provide an accurate and comprehensive view of your finances so you can move forward with confidence.

The Importance of Catch-Up Bookkeeping

You might be wondering—if I’ve already fallen behind, why bother catching up at all? Can’t I just pick up from where I left off and move forward? The answer is no, and for good reason.

Neglecting to catch up on your financial records can have significant consequences. It’s not just about maintaining clean records; it’s about protecting your business or personal finances from potential pitfalls.

Avoiding Legal and Tax Consequences

The first and most obvious reason to catch up is to avoid legal and tax-related issues. In many countries, businesses are legally required to maintain accurate and up-to-date financial records. These records are used to file taxes, provide financial statements to stakeholders, and comply with government regulations.

When your financial records are incomplete, you risk missing tax deadlines, underreporting income, or failing to deduct expenses accurately. This can lead to penalties, fines, or even audits from tax authorities.

Take, for example, a small business owner who hasn’t updated their books in over a year. When tax season arrives, they scramble to gather information, but they don’t have a clear record of all their expenses. They end up overpaying on taxes, simply because they can’t account for deductible expenses. In a worst-case scenario, they could be audited, leading to a stressful and expensive investigation.

By catching up on your records, you ensure that everything is accounted for when it comes time to file taxes. You’re also safeguarding yourself against legal repercussions by ensuring that your business complies with regulations.

Informed Decision-Making

Beyond tax compliance, having accurate financial records allows you to make informed decisions about your finances. Whether you’re managing a business or personal budget, knowing exactly where your money is coming from and where it’s going is essential for strategic planning.

Imagine trying to run a business without knowing how much revenue you generated last quarter, or how much you spent on inventory. Without that data, you’re making decisions in the dark. You might overspend, underinvest, or miss out on opportunities for growth simply because you don’t have a clear understanding of your financial situation.

With catch-up bookkeeping, you regain that clarity. You’ll have the data you need to:

- Set realistic financial goals

- Adjust your pricing strategy

- Identify cost-saving opportunities

- Make investment decisions

For individuals, catching up on financial records means being able to budget more effectively, plan for future expenses, and make better decisions about savings and investments.

Maintaining Relationships with Lenders and Investors

If you’re seeking external funding for your business—whether through loans, investors, or grants—having up-to-date financial records is non-negotiable. Lenders and investors want to see accurate financial statements that reflect your business’s performance. Incomplete or outdated records can signal poor financial management, which can make lenders or investors hesitant to provide funding.

Catch-up bookkeeping helps you present a professional and organized financial picture. It shows that you take your financial responsibilities seriously and that your business is in a stable position to grow.

Now that we’ve established the importance of catching up on your financial records, let’s dive into the process itself. Depending on the extent of the backlog, this process can range from relatively simple to complex. However, with the right approach, it’s entirely manageable.

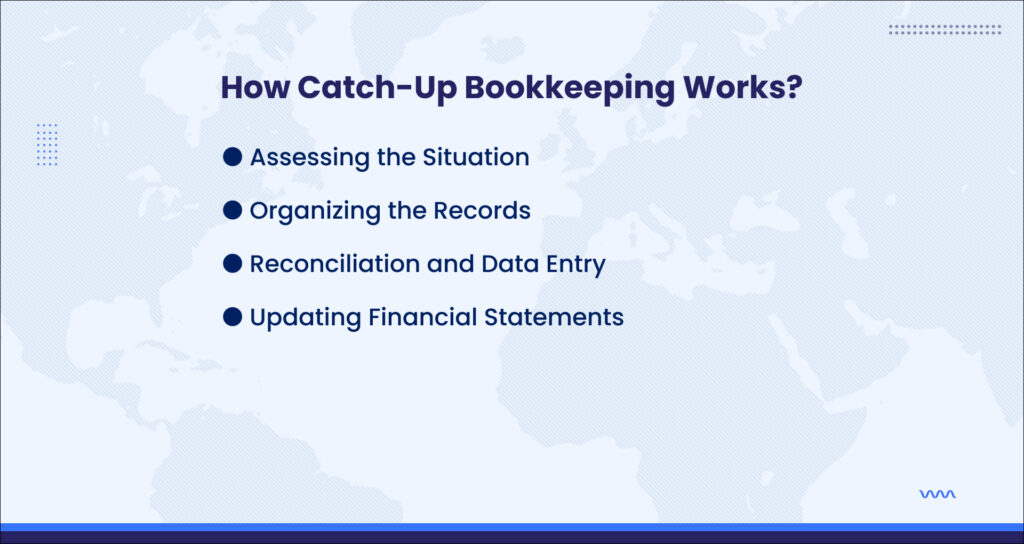

Assessing the Situation

The first step in the catch-up process is assessing how far behind you are. This involves taking stock of your financial records and identifying the gaps. How many months (or years) of financial data are missing? Are there specific periods where your records are incomplete, or have you fallen behind on all aspects of tracking?

This is where you’ll need to gather all relevant documents, including:

- Bank statements

- Credit card statements

- Invoices and receipts

- Payroll records (for businesses)

- Tax returns (for individuals or businesses)

The goal is to identify what’s missing and create a plan to fill in the gaps.

Organizing the Records

Once you’ve assessed the situation, the next step is organizing the financial documents. This is where many people feel overwhelmed, especially if their records are scattered across various platforms, accounts, or even physical documents. But organizing is crucial—without a clear system in place, catching up becomes much harder.

You’ll need to categorize your transactions based on income, expenses, assets, and liabilities. For businesses, this may also involve categorizing expenses by department or project. The more organized you are at this stage, the smoother the reconciliation process will be.

Reconciliation and Data Entry

After organizing the records, it’s time to begin the reconciliation process. This involves matching the transactions on your bank and credit card statements to your financial records, ensuring that everything is accounted for. If you’re missing transactions, now is the time to find and record them.

In this phase, accuracy is key. You’ll want to double-check that every transaction is recorded correctly, with the appropriate category and date. Errors in reconciliation can lead to an inaccurate financial picture, so take your time to ensure everything matches up.

For businesses, this may also involve reconciling payroll, invoices, and inventory records to ensure that your financial statements are accurate.

Updating Financial Statements

Once the reconciliation process is complete, you can begin updating your financial statements. This includes income statements, balance sheets, and cash flow statements. For individuals, this may involve updating your personal budget, tracking savings, and recording investments.

These statements provide a snapshot of your financial health, and updating them gives you the clarity needed to move forward.

Real-World Examples of Catch-Up Bookkeeping

Let’s take a look at some real-world scenarios where catch-up bookkeeping made a significant difference in the financial well-being of individuals and businesses.

Example 1: Small Business Owner

Tina owns a boutique clothing store. For the first few years, she managed her finances on her own using spreadsheets and simple accounting software. However, as her business grew, her transactions became more complex, and she found herself falling behind on her bookkeeping. By the time tax season rolled around, she was months behind on updating her records.

Tina’s accountant recommended catch-up bookkeeping. Over the course of a few weeks, Tina and her accountant worked together to organize her financial documents, reconcile her bank statements, and update her financial records. Once the process was complete, Tina had a clear understanding of her business’s financial health, and she was able to file her taxes accurately and on time.

More importantly, Tina used the insights gained from the process to make strategic decisions about inventory management and marketing, leading to increased profits the following quarter.

Example 2: Freelance Writer

David is a freelance writer who works with multiple clients across various industries. While he’s great at managing his creative projects, he struggles with financial management. Over the course of a year, David fell behind on tracking his income and expenses, and by the time he realized the extent of the backlog, he was facing an audit from the tax authorities.

David hired a financial professional to help him with catch-up bookkeeping. Together, they gathered his invoices, bank statements, and receipts, and worked to reconcile his financial records. Once his books were up to date, David was able to provide accurate financial statements to the tax authorities and avoid penalties.

The process also gave David valuable insights into his cash flow, allowing him to better plan for future expenses and investments in his freelance business.

Wrap Up

Falling behind on financial records can feel like a daunting problem, but with the right approach, it’s entirely manageable. Catch-up bookkeeping offers a practical solution for those who want to regain control of their finances, whether they’re running a business or managing personal budgets.

By taking the time to organize your records, reconcile transactions, and update your financial statements, you’ll not only avoid potential legal and tax issues, but you’ll also gain valuable insights into your financial health. The Pro Accountants can play a significant role in making the process more efficient, but ultimately, it’s about taking action to bring your financial records up to date.

Remember, the goal isn’t just to catch up—it’s to create a foundation that allows you to maintain ongoing financial clarity. With your books in order, you’ll be in a much stronger position to make informed decisions, plan for the future, and achieve your financial goals. So, schedule your meeting now!